The sell off in Markets in early August certainly triggered some panic, especially among leveraged traders and anyone short the Yen. It also led a number of allocators to raise concerns based around Analogues from previous Augusts, notably 2000, when a similar small rise in Japanese rates crashed the Dot Com bubble, but also 1998, when the Russia default blew up LTCM (the so called smartest guys in the room). August certainly doesn’t have great seasonality, (apart from 2020) but we suspect that what we are seeing here is an unwind of the three big anomalies we have been highlighting for a while; the concentration risk in US Equities, the very low level of the VIX and the extreme undervaluation of the Japanese Yen. And the possible appearance of a new anomaly - the flight to quality in US Bonds is being explained as a recession signal, along with calls for the long awaited Fed Pivot. We doubt it will result in either.

Last week in the August monthly Market Thinking piece, we highlighted the role of the Yen carry trade unwind in market instability. At the time, the widespread observation from the commentariat was that the early August sell off in markets was to do with ‘recession fears and US jobs numbers’, but long experience tells us that sharp market moves are very rarely about economics, they are almost always about internal dynamics.

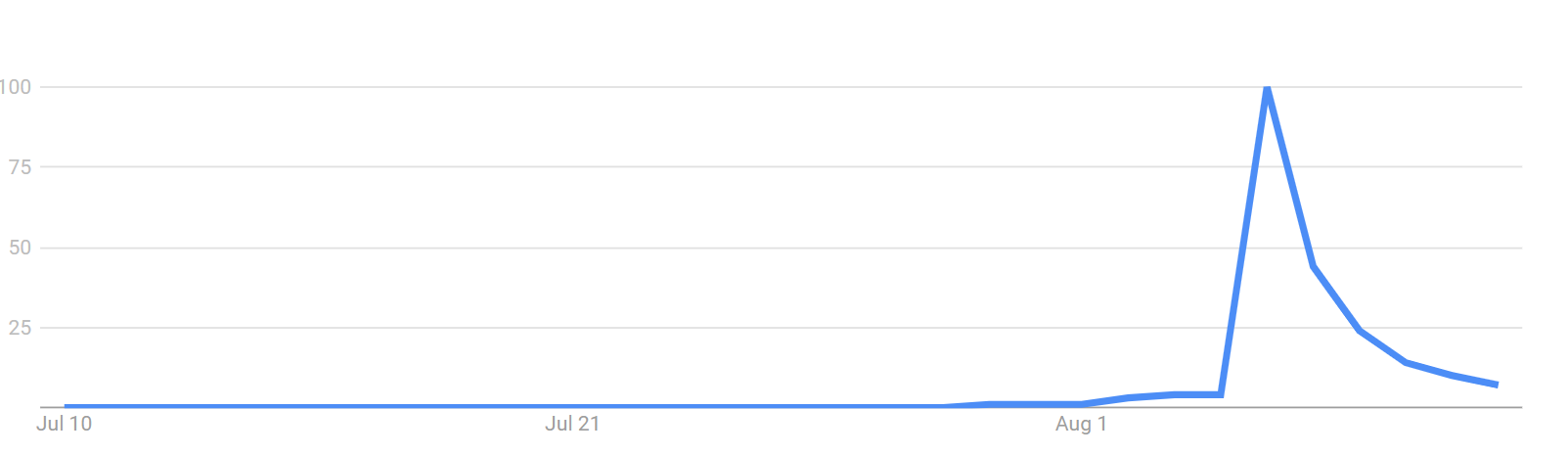

Some of the most dramatic moves were in Japan, where the Nikkei saw the second biggest down day since 1950, while the TOPIX was even worse than the 1987 crash (which was also a market mechanics rather than an economic situation). As such, the pundits’ attention moved away from claiming it was all about US economic data (to the majority of the macro world, the US bond market is their hammer and thus everything looks like a nail) and the expression Yen carry trade started to trend as shown in the Google Trends graph.

US Google Trends on the term Yen Carry Trade.

As we pointed out in the monthly, the Japan selling was likely associated with a sharp upward move in the Yen and the fact that many international investors who had been piling into Japan of late had been doing so using ETFs that were hedged back into $. The rise in Japanese rates at the end of July and the sharp rally in the currency, together with aggressive comments from the Japanese authorities about the value of the Yen were enough to trigger some stop losses and, in thin markets, this was enough to cascade through markets. The BoJ quickly stepped in to calm markets and they have largely stabilised if not yet fully recovered, highlighting that the BoJ, like the Fed and other central banks spends far more of its time looking at financial stability than the High Frequency Macro data that so obsess the Bond Markets.

However, this selling wasn’t limited to Japan, which is why the world noticed and also why it is nervous. For decades, the Japanese have been a key source of market liquidity - often attributed to ‘Mrs Watanabe’ chasing yield wherever it can be found around the world. Muscle memory of previous Japanese rate hikes (particularly 2000 and 2007), and the impact they have on western markets as that liquidity is withdrawn, are enough to make experienced traders nervous, especially as the liquidity injected by the Fed and, more recently, the Treasury is also tightening.

In August 2000, the Japanese raised rates by 25bp and the Dot Com bubble burst. In February 2007, they raised rates and we saw the start of the Financial Crisis.

The wider concern is that the Yen carry trade had extended to non Japanese borrowing in Yen to fund momentum trades into the US equity market and it is this unwind that we are now observing. Certainly our model portfolios saw risks rising in momentum stocks at the end of July and the fact that almost 70% of stocks outperformed the S&P500 in July (i.e. beat the so called M7) suggests de-leveraging and de-risking was already taking place. If, as we all now suspect, some of that leverage was in Yen, then it has simply sped up the process of unwinding the other anomalies.

The August 2000 Analogue

However, it has certainly dented the AI bubble and those worried about the August Analogue from 2000 are adding it to their chart of Cisco 2000 versus Nvidia 2024 (chart courtesy of our friends at Redburn Atlantic).

This shift in sentiment was also not helped by veteran Tech stock Intel issuing what amounted to a profit warning leaving it down 40% down on the month and almost 60% ytd and a general recognition that the bonanza from AI might not be actually arriving for a while. As we noted last August, with the exception of perhaps Nvidia, the rally in the Tech stocks around the excitement of AI also had to be put in the context of the massive selloff in the previous 12 months, such that on a two year view longer term investors in say Microsoft are up, but ‘only’ 20%, that net gain only coming since q4 last year. This is different to the 2000 era (again with the possible exception of Nvidia) and what we are seeing at the moment is leveraged traders bailing out generally (note the drop in Bitcoin), no t because they see any issue with the US economy, but because their margin is being called. A reset not a recession

The third anomaly- the persistent low level of VIX - was also reversed, as it jumped dramatically in early August - notionally by 42 points on Monday - to levels almost as high as when Covid hit. Sometimes called the Fear index, we prefer to think of it as the price of put options and in that sense the spike probably said as much about thin markets as a rush by asset allocators to ‘buy protection’. More likely a rush by those who had been selling puts to close out their position.

The 1998 Analogue

The rush to unwind derivative positions reminds us of another August debacle - the August 1998 Russia default and the blow up of Long Term Capital Management a hedge fund with lots of PhDs and Professors of Finance, but, as the wags said at the time, were not long term and had no capital management. Indeed they were largely playing the game of ‘picking up nickels in front of a steam roller’ - lots of small trades with a small probability of failing, but a catastrophic result if they did.

We like this analogue for several reasons. First, it came against a background where the US had hugely out-performed Emerging Markets over the previous 12 months (+20% versus -40%), second the selloff was an internal market dislocation of distressed sellers and forced buyers and not anything to do with economics. And third, the flight to safety into US Treasuries (exaggerated by the fact that LTCM and all its clones were short) was widely misinterpreted by the macro pundits with the proverbial hammer as evidence of an upcoming recession. Indeed I had some powerful ‘disagreements’ with macro colleagues back then and their ‘Economic Armageddon’ call.

For context, these were the market moves in August/September 1998

- S&P 500 -15.4%

- Small Caps (S&P 600) -25.5%

- Mid Caps (S&P 400) -21.8%

- Emerging Markets (MSCI EM) -26.7%

- Foreign Stocks (MSCI EAFE) -11.5%

But then these were the total returns from September 1998 through March 2000:

- S&P 500 +59.8%

- Small Caps (S&P 600) +48.4%

- Mid Caps (S&P 400) +81.2%

- Emerging Markets (MSCI EM) +113.9%

- Foreign Stocks (MSCI EAFE) +49.0%

Needless to say, there was no economic Armageddon. Economist Paul Samuelson once quipped that the Stock Market had called nine of the last five recessions. That was back in September 1966 after (you guessed it) a sharp selloff in August of that year and led to a new bull market in 1967, just as 1998 led to a bull market in 1999. This is not to be dismissive, rather to tweak Samuelson’s comment and say that “Bond economists have used evert notable sell off in equities to call for a recession and thus a bull market in bonds”.

A New Anomaly - the Pivot is back.

The flight to safety this last week has once again pushed US 10 Year yields below 4% and, as ever, this is being treated as a ‘signal’ that the smart guys in bonds know something that the dumb guys in equities don’t. The CBOE rate watch indicator has just swung from a near 70% probability of no rate cut or even an increase by year end (in July) to now, apparently, there being no chance of anything less than a 50bp cut, with a 30% chance of more than 100bp. This is the ‘pivot’ excitement all over again.

Of course, this indicator is as ‘unreliable’ as the VIX, it tells us the cost of hedging against that probability rather than the likelihood of it actually happening, but anyone buying bonds on the back of it needs to be very careful - the low probability of rate cuts last year (when bonds were yielding 5%) were equally and oppositely incorrect. As we noted in the monthly, cutting rates will help the government paying almost 20% of its discretionary Budget out in debt interest, but have little impact on US consumers, who have fixed mortgages that are not worth re-fixing unless long term rates drop below 3%. As such cuts will not help growth, but they would lead to an even bigger sell-off in the $ and exaggerate financial instability. Having just watched the BoJ, the Fed are not going to risk anything more than a small cut.

Clearly at the moment, the $ markets don’t believe the Bond markets, making the $ a key variable to watch.

To conclude

The recent selloff is now widely acknowledged to be due to an unwind of the Yen Carry trade rather than anything economic, although the Bond markets, as ever, are trying to use the disruption to force a cut in interest rates and push the narrative of a recession. We suspect that while the top is probably in for the year in US equities, so too is it in bonds, but the former do not have the conditions for a new bear market, while the latter have not got the conditions for a new Bull market.

The August 1998 analogue (or even the 1966 one at a stretch) looks to us better than the August 2000 one, with equities rebounding but more aggressively in the areas that had been relatively left behind before the market sell-off. The anomalies of the ultra low Yen and heavily focussed S&P500 appear set to unwind further, while the ultra low levels of VIX have also reset. The anomaly now (in our view) is the idea of a bull market in US bonds with a mid/late cycle deficit of 6% of GDP and no external appetite for US paper. The yield curve is now flat, but is now pricing in an unlikely level of rate cuts by the Fed.